Reorg delivers critical data and analysis for leveraged finance and restructuring professionals.

In this paper, access a curated selection of data-driven insights into credit situations developing around the world right now.

March 31, 2023

Reorg’s expert global team research and publish thousands of analysis and intelligence articles every year to bring clarity to investors, bankers, lawyers and consultants. We’re obsessed with providing actionable insight on the sub-investment grade credit markets.

Here are some examples of coverage through the credit lifecycle from performing and primary markets to distressed, restructuring and post-reorg that you and your team could access through a subscription to Reorg. If you are interested in understanding how a Reorg subscription can benefit your business, request trial access here www.reorg.com/trial.

Americas

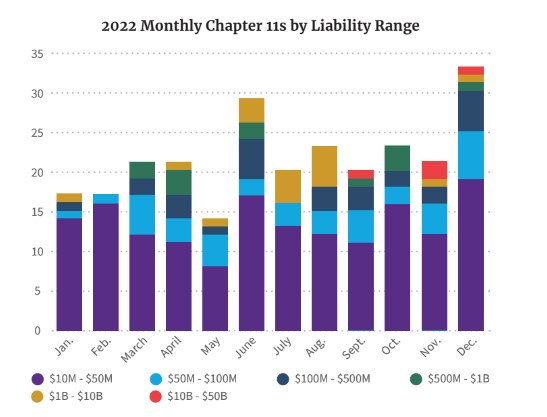

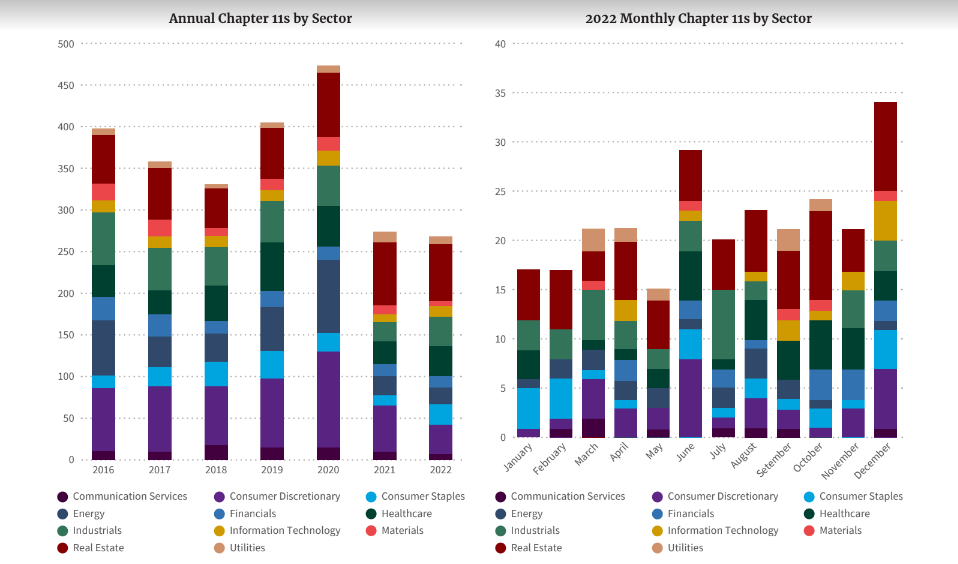

In the U.S., 19 debtors filed for chapter 11 protection over the past two weeks, according to Reorg’s First Day Database; seven of those names came to court with liabilities in excess of $100 million. Some of the fears surrounding contagion from SVB Financial’s collapse have begun to abate, as shown by a slight uptick in primary market activity, as two bond deals and several leveraged loan transactions came to market. Nevertheless, regional banks remain a focus, and Reorg’s analyst team commenced coverage of some of the most prominent among them. The possibility of an economic slowdown remains a focus, as investors wait for signs that the Fed’s tightening program is taking effect amid expectations that the central bank will hike rates again this year as inflation remains stubbornly high. Advisor mandates are also increasing, as the impact of higher rates on floating-rate debt saps cash flows.

Fundamentals by Reorg: Reorg’s Fundamentals and ESGx analyst teams launched their debut report on Zayo this week. Our report includes the following sections: Capital Structure, Forecasts and Leverage Trajectory, Comparables and Industry Dynamics, ESG, Financial Overview, Business Overview and M&A Strategy. Access is limited to Zayo lenders, bondholders or parties under an NDA.

Citrix Systems: Bookrunners for Citrix Systems’ $3.95 billion SOFR+700 bps second lien bridge loan began talking to a select group of funds late last year about a potential takeout of the software company’s bridge loan with new paper yielding about 14%. The structure and pricing have yet to be finalized, but the banks have some time, as the bridge does not expire until October. However, in light of risks associated with the company, the yield could widen to as much as 16%. Read more on Citrix Systems.

U.S. Regional Banks: The Americas credit analyst team has initiated coverage of nine regional banks that have come into focus since the collapse of Silicon Valley Bank: Zions Bancorp, KeyCorp, BankUnited, HomeStreet Capital, SVB Financial Group, Signature Bank, First Republic, PacWest Bancorp and Western Alliance. Read more.

Shoes For Crews: A group of lenders to Shoes For Crews’ $258 million L+500 bps first lien term loan B has organized with King & Spalding, according to sources. The Boca Raton, Fla.-based provider of slip-resistant footwear for various industries, including food service, retail and industrial workers, has struggled with high leverage and weak performance during the Covid-19 pandemic.

Western Global Airlines: an Estero, Fla.-based cargo carrier, has hired Weil Gotshal, Evercore and FTI Consulting as legal counsel and financial advisors, respectively, as the company contends with tightening liquidity, a pilot shortage and operational challenges amid the slowing air cargo market. The company’s bondholders are working with Ducera Partners as financial advisor, and an upcoming $21 million coupon payment in August is in focus.

Americas Municipals

Puerto Rico Electric Power Authority: The judge overseeing the Title III restructuring of the Puerto Rico Electric Power Authority, or PREPA, delivered a critical opinion on bondholder liens ahead of a confirmation trial scheduled for July. Judge Laura Taylor Swain’s decision noted that the bondholder’s lien was limited to a $16 million sinking fund, but that bondholders of PREPA debt had recourse through an unsecured net revenue claim. Uninsured bonds traded up on the news from the high 60s to low 70s, indicating a potential settlement ahead of confirmation. Parties to the dispute have filed a joint statement outlining their views on the next steps in PREPA’s restructuring. Read more.

American Rescue Plan Act: The state of Ohio filed a petition for writ of certiorari with the U.S. Supreme Court seeking review of a November 2022 opinion by the Sixth Circuit holding that Ohio’s challenge to the offset restriction provision, or tax mandate, of the American Rescue Plan Act, or ARPA, which prevents states from using ARPA funds to directly or indirectly offset net reductions in tax revenue resulting from changes in state law, was mooted by a clarifying regulation issued by the Treasury Department.

Ohio asks the Supreme Court to answer whether federal courts still have jurisdiction to adjudicate states’ challenges to the tax mandate in light of the clarifying regulation and whether the tax mandate is unconstitutional, arguing that the provision is unconstitutionally ambiguous and coercive. In January, the Supreme Court denied a similar petition by Missouri seeking review of an Eighth Circuit determination that the state lacked standing. Read more.

Europe

In Europe, additional tier 1 bond investors are still aching from a controversial decision announced on Sunday evening, March 19, by the Swiss financial regulators to wipe out $17 billion of Credit Suisse AT1 debt as part of a merger with domestic rival UBS. The move sent shockwaves through the markets because the regulators allowed Credit Suisse shareholders, junior to AT1 creditors, to walk away from the imploding bank with a small minority equity stake, valued at $3 billion, in the new, much larger UBS – thereby disregarding the absolute priority rule. Global litigation firms are now in full swing to prepare legal challenges.

Credit Suisse: Law firms are preparing multiple litigation strategies to push back on Switzerland’s March 19 decision to write CHF 16 billion of Credit Suisse additional tier 1 debt down to zero. Quinn Emanuel and Pallas Partners are both pitching disgruntled investors, trying to build a large enough group to lead the charge in Switzerland, which, according to Pallas’ Natasha Harrison, has “annihilated its reputation as a safe haven.” Reorg’s legal analysis shows that Credit Suisse’s AT1 bond documentation does allow for the regulator to write down the subordinated debt in a non-liquidation scenario. Read more.

Deutsche Bank’s additional tier 1 notes fell 8% to 10% on March 24, the most hit in Europe, as policymakers are struggling to calm waters after the 16 billion Swiss franc ($17.4 billion) vaporization of Credit Suisse AT1s. The German lender’s shares are down 10%, while its five-year credit default swap was indicated at 302 basis points last Friday, March 24, up 18% compared with the day before. The banking sector, as well as broader markets, have fallen because of the turmoil caused by the collapse of three U.S. regional banks and the last-minute merger between Credit Suisse and UBS, in which the former’s AT1 notes were wiped out completely and its equity took a big loss but were not fully written down. Read more.

Flint Group said more than 75% of first lien debt lenders by value and 90% of second lien debt lenders have acceded to a lockup agreement for its recapitalization deal. The Luxembourg-based printing and packaging company added that it expects this level of support to enable the group to implement the transaction by way of a U.K. scheme of arrangement. The transaction will cut debt by €740 million and reduce interest costs by €75 million in financial year 2023. Lenders will provide €72 million of new liquidity and extend maturities by up to four years. The transaction would cut operating group debt by more than 50% through a partial restatement of the first lien debt, with the rest of the first and second lien pushed up into new holdco debt. Read more.

Codere: Spanish gaming company Codere, which previously restructured its debt in 2020 and 2021, said it intends to raise €100 million of super senior new money, and defer interest due under its 2026 and 2027 PIK super senior notes and principal under its 2026 PIK super senior notes. The group is using a consent solicitation to implement the key terms of the deal, requiring the consent of just 50% of each note’s tranche and in addition launching an exchange offer. The company is dealing with a significant interest burden, which is eroding its liquidity. As of the nine months ended Sept. 30, 2022, the group’s total cash interest burden amounted to €68.4 million, of which €44.3 million related to bond net cash interest payments. Including PIK interest of €61.5 million, total interest amounted to €129.9 million. Read more on Codere.

Tricor/Vistra: Investors who considered the $1.66 billion-equivalent incremental term loan B being marketed to support the merger of corporate services companies Tricor and Vistra highlighted that the company’s scale will more than double as a result of the deal. Both businesses are based in Hong Kong and have activities in Asia, however Vistra’s activities in the EMEA region and in the Americas will enable Tricor to expand its focus beyond Asia. Relatively low capex also means that free cash flow generation is strong, investors said. The deal comes with significant execution risk and large integration costs. Additionally, the two companies may have overlapping activities and clients. The dollar portion of the deal priced at SOFR/Euribor+ 475bps with a 97.5 OID.

Quark: Arcano Partners has been appointed to run the sale of Spanish consulting and engineering company Quark, sources told Reorg. The founders of Quark are looking for a new partner to continue the company’s growth and international expansion.The process is at an early stage, sources noted.

Asia

In Asia, earnings were a focus for investors. CIFI Holdings started negotiating with holders of its over RMB 2B onshore bond to cancel a put option, and Reorg began coverage of Chindata Group.

Logan Group: We dialed into a conference call held by the company’s chief restructuring officer, who told investors that Logan aims to distribute a detailed restructuring proposal to all creditors in the next few weeks, and that the terms will feature amortization payments throughout the extended period. Read more.

China Evergrande: Reorg compares key terms of recent liability management and restructuring exercises launched by Chinese real estate developers against the proposed restructuring terms under China Evergrande Group’s restructuring term sheet. Among other details, we highlight the three schemes under the plan and benchmark various terms against historical and ongoing restructurings such as the restructuring consideration, debt/equity swap terms, money terms, asset sales undertaking and credit enhancements. Read more.